The Threat You’re Already Tracking

Most PEG station managers know the first number: U.S. cable TV subscriptions dropped from 96 million in 2017 to roughly 68 million in 2024. Franchise fee revenue followed. Stations like Nashua Community Television saw revenue fall from $483,000 to $383,000 over seven years, a 21% decline. Portsmouth Public Media TV dropped from roughly $130,000 to $86,000 in a single year.

This is Cord Cutting 1.0. It’s real, it’s painful, and most PEG stations have at least started to plan for it. But the full PEG station funding crisis runs deeper than TV subscriber losses.

There’s a second number that changes the math entirely.

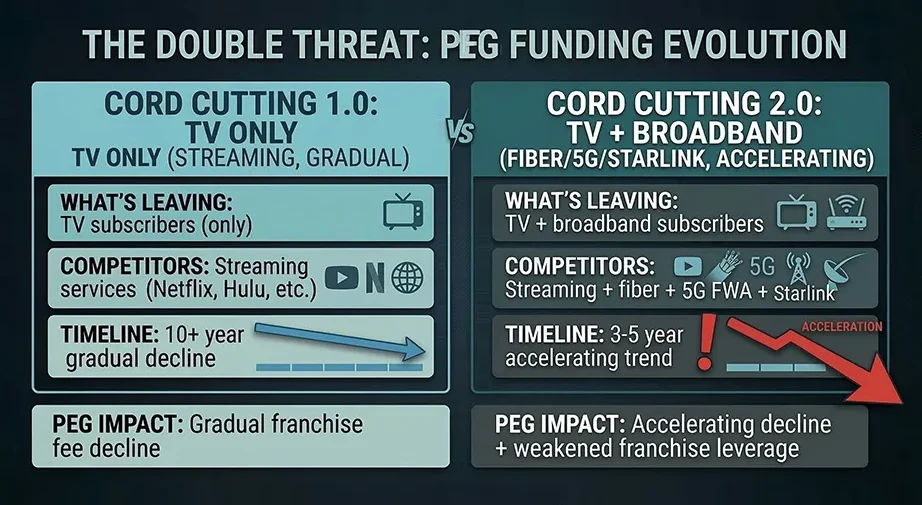

What Is Cord Cutting 2.0?

Cord Cutting 2.0 refers to the loss of cable broadband subscribers (not just TV subscribers) to fiber, fixed wireless (5G), and satellite competitors like Starlink. For PEG stations, this creates a second funding threat beyond traditional cord-cutting, one that compounds the franchise fee decline already underway.

| Cord Cutting 1.0 | Cord Cutting 2.0 | |

| What’s leaving | TV subscribers | TV + broadband subscribers |

| Competitors | Streaming services | Streaming + fiber + 5G FWA + Starlink |

| PEG impact | Gradual franchise fee decline | Accelerating decline + weakened franchise leverage |

| Timeline | 10+ year trend | 3-5 year acceleration |

The Threat You’re Probably Not Tracking

In 2025, Comcast and Spectrum, the two largest cable operators in the U.S., lost a combined 1.11 million internet customers. Not TV subscribers. Internet subscribers.

Cable broadband, the product line that was supposed to be cable’s durable revenue engine, is losing customers to three competitors simultaneously:

- Fixed wireless (5G home internet): T-Mobile, Verizon, and AT&T added roughly 3.8 million FWA subscribers in 2025. T-Mobile alone now has 8.5 million fixed wireless customers, making it the fifth-largest residential broadband provider in the country.

- Fiber: AT&T passed 10 million fiber subscribers in 2025, with fiber revenue growing 16.8% year-over-year. Verizon is acquiring Frontier to reach 29 million fiber passings.

- Starlink: SpaceX’s satellite internet service reached roughly 2.6 million U.S. subscribers by late 2025, doubling its global subscriber base in a single year.

Charter’s CEO has said publicly that he is not predicting broadband subscriber growth in 2026. S&P Global’s 2025 industry credit outlook describes the cable industry as “bundling up for subscriber losses.”

This is Cord Cutting 2.0.

![]()

Why Broadband Losses Matter for PEG Stations

Cable broadband subscriber losses threaten PEG station funding in three ways: accelerating TV subscriber churn through bundle cancellations, reducing cable operator incentives to maintain PEG obligations at franchise renewal, and weakening municipal leverage over cable operators.

A reasonable objection: franchise fees are calculated on cable video revenue, not broadband revenue. The Cable Communications Act of 1984 caps the fee at 5% of gross cable video revenues. Broadband is explicitly excluded under the FCC’s “mixed-use rule.”

So why should PEG stations care about broadband subscriber losses?

Three reasons.

- Bundling economics. Cable operators sell TV and internet as bundles. When a household cancels broadband for fiber or 5G, they often cancel TV too. Broadband losses accelerate TV subscriber losses, which directly reduce franchise fee revenue.

- Operator leverage at renewal. When a cable company’s total subscriber base in a municipality shrinks, the operator has less to lose by walking away from franchise obligations. PEG requirements are negotiated items in franchise agreements. A cable operator serving 40% of households has more incentive to maintain PEG obligations than one serving 15%.

- Reduced political leverage for cities. Municipalities use franchise agreements as leverage: the cable company gets access to public rights-of-way in exchange for franchise fees and PEG support. As cable loses market share to fiber and wireless competitors that don’t require franchise agreements, the cable franchise itself becomes less valuable, and the leverage cities hold over cable operators weakens.

The Math Is Moving Faster Than Most Budgets

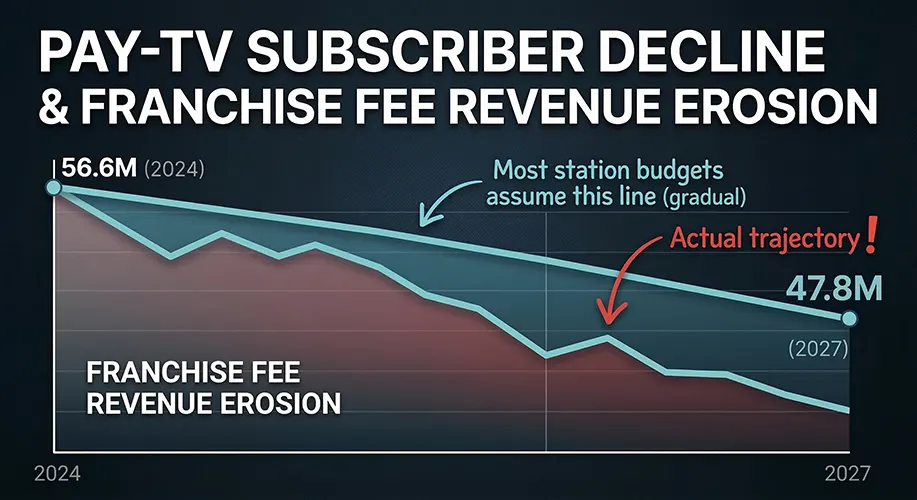

The financial models most stations use were built on a single assumption: TV cord-cutting as a gradual, linear decline. That assumption was reasonable when broadband subscriber data wasn’t available at the market level. But the broadband loss trend only became visible in 2024-2025 earnings reports, and most station budgets haven’t been updated to reflect it.

Consider the timeline:

- Pay-TV subscribers are projected to fall from 56.6 million (2024) to 47.8 million by 2027, a 15% decline in three years.

- Pay-TV revenue in North America peaked at $111 billion in 2015 and is forecast to fall to $62 billion by 2027.

- Over 10 cable TV networks are expected to shut down in 2026 alone.

Layer broadband losses on top of that, and the picture changes from a gradual decline to an accelerating one.

What PEG Stations Can Do Now to Prepare

The stations that survive this transition will be the ones that act before the next franchise renewal cycle.

Audit your franchise fee projections. If your budget model assumes a linear decline based on TV cord-cutting trends, it’s probably too optimistic. Factor in broadband subscriber losses and the compounding effect on cable operator revenue.

Build your data case now. When franchise fees shrink, the argument for PEG funding has to come from somewhere else: demonstrated community reach, documented engagement, measurable civic impact. Blue Astral’s 2025 PEG Digital Readiness Study found that 53.4% of PEG stations lack the analytics infrastructure to make this case. That’s a fixable gap, but it takes time to build the data history that makes the argument credible.

Track the broadband franchise fee debate and get involved. Representatives from Philadelphia, Seattle, and Minneapolis met with FCC officials in January 2026 to push for extending franchise fees to cable broadband revenue. If the “mixed-use rule” is repealed, broadband franchise fees on the estimated $75 billion in annual cable broadband revenue could generate $3.75 billion for municipalities. Follow the Alliance for Community Media advocacy updates, submit public comments during FCC rulemaking periods, and coordinate with your municipal government on franchise renewal strategy. Stations that have already built digital infrastructure and can demonstrate audience value will be better positioned to argue for a share of that new revenue.

Explore alternative funding models. Some states are already moving. Vermont allocated $1 million to the Vermont Access Network through its FY2025 appropriations. Massachusetts legislators are considering a 5% fee on streaming companies to fund community media. These efforts are early, but they signal a direction.

The Counterargument: Broadband Fees Could Save Everything

The strongest objection to this analysis: if the FCC repeals the mixed-use rule and extends franchise fees to broadband revenue, the $3.75 billion in potential new municipal revenue could more than offset TV subscriber losses. Some states are already experimenting with streaming taxes.

That’s a real possibility. But regulatory change is slow, politically contested, and not guaranteed. Vermont’s $1 million allocation and Massachusetts’ streaming fee proposal are promising signals, not reliable budget assumptions. Stations that plan their next 3 years around hypothetical regulatory wins are taking a risk. Stations that build their data case and diversify their funding arguments now are positioned to benefit from regulatory change if it comes, and to survive if it doesn’t.

The Bottom Line on the PEG Station Funding Crisis

Cord Cutting 1.0 was about TV subscribers leaving cable. PEG stations felt it as a slow revenue decline.

Cord Cutting 2.0 is about the entire cable ecosystem shrinking: TV, broadband, and the franchise agreements that depend on both. The timeline is faster, the revenue impact is deeper, and the political leverage that cities have to protect PEG funding is weaker.

Stations planning for a 5-year gradual decline may have closer to 3 years before the math becomes unworkable. The ones that build their data case, diversify their funding arguments, and invest in digital infrastructure now will be the ones that survive.

Blue Astral helps PEG stations turn community impact into the measurable data that secures funding. See where your station stands before your next franchise renewal.

FAQ

Q: How do cable broadband losses affect PEG station funding?

A: Cable broadband losses accelerate TV subscriber churn (customers who cancel internet often cancel TV too), reduce cable operators’ incentive to maintain PEG obligations during franchise renewals, and weaken the leverage municipalities use to negotiate franchise fees and PEG support.

Q: What is Cord Cutting 2.0 and why does it matter for community media?

A: Cord Cutting 2.0 refers to the loss of cable broadband subscribers to fiber, fixed wireless 5G, and satellite competitors like Starlink. It matters for community media because it compounds the franchise fee decline from TV cord-cutting, shrinking the entire cable ecosystem that PEG funding depends on.

Q: Can broadband franchise fees replace lost PEG station revenue?

A: If the FCC repeals the “mixed-use rule,” franchise fees on the estimated $75 billion in annual cable broadband revenue could generate $3.75 billion for municipalities. But regulatory change is slow, politically contested, and not guaranteed. Stations should not plan their budgets around this outcome alone.

Q: How fast are PEG stations losing franchise fee revenue?

A: Documented declines range from 21% (Nashua Community Television over seven years) to over 30% (Portsmouth Public Media TV in a single year). Pay-TV subscribers are projected to fall from 56.6 million in 2024 to 47.8 million by 2027, a 15% decline in three years. Stations planning for a 5-year gradual decline may have closer to 3 years before the math becomes unworkable.

Sources:

- Cord Cutters News – Comcast and Spectrum 2025 subscriber losses – Jan 2026

- Cord Cutters News – Spectrum full year 2025 results – 2026

- Fierce Network – Big 3 FWA capacity for 32M customers – 2025

- IEEE ComSoc – AT&T fiber growth – April 2025

- Broadband Breakfast – Starlink US subscriber base – 2025

- Nashua Ink Link – NH franchise fee declines – 2024

- Granite State News Collaborative – NH stations scramble for funding – Nov 2024

- CableCompare – Cable TV subscriber projections – 2026

- Evoca – Cable TV statistics – 2026

- Broadband Breakfast – Big cities push FCC on broadband franchise fees – Jan 2026

- S&P Global – Cable industry subscriber loss outlook – 2025